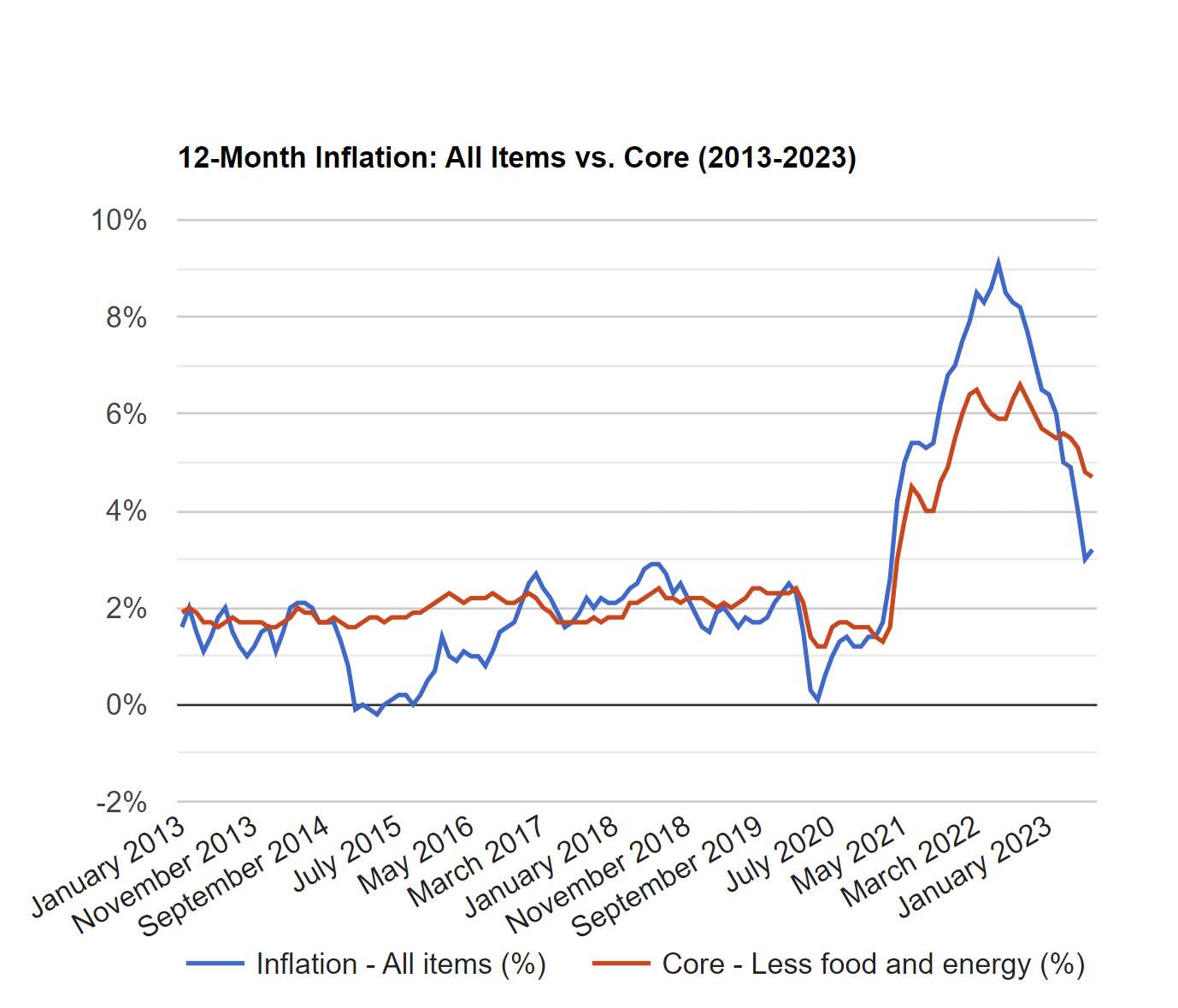

The year 2022 was a bloodbath for both equity and bond markets–the S&P 500 was down 18% and the Bloomberg US Aggregate Bond Index had its worst year ever, down 13%. This year, 2023, began with the US debt ceiling standoff, followed by a banking crisis, and continued rate hikes by the major central banks. The economy seemed like it would get worse before it got better, and the consensus was calling for a near-term recession. However, the stock market quickly shrugged off many of these concerns. Year-to-date as of August 31, the S&P 500 is up approximately 17% and NASDAQ is up approximately 34%. The S&P 500 is officially in a bull market (i.e., up at least 20% from its recent lows in October 2022). With the Federal Reserve and some economists no longer forecasting a recession[1], it makes one wonder what has changed in the last few months.

From the market’s perspective, here is what went right:

On the surface, these events are very encouraging, but if we look more closely, not everything is as promising as it seems:

Along with the issues mentioned above, the fiscal and monetary policies implemented in the last few years are still working through the system (and at times, the two work against each other), which makes efforts at timing the market increasingly challenging. The first eight months of this year are a solid reminder of the benefits of maintaining a disciplined, long-term investment plan.

Please do not hesitate to reach out if you have questions or would like to discuss your own situation.

[4] Strategas

Disclosures

This material is solely for informational purposes and shall not constitute a recommendation or offer to sell or a solicitation to buy securities. The opinions expressed herein represent the current, good faith views of the author at the time of publication and are provided for limited purposes, are not definitive investment advice, and should not be relied on as such. The information presented herein has been developed internally and/or obtained from sources believed to be reliable; however, neither the author nor Manchester Capital Management guarantee the accuracy, adequacy or completeness of such information. Predictions, opinions, and other information contained in this article are subject to change continually and without notice of any kind and may no longer be true after any date indicated. Any forward-looking predictions or statements speak only as of the date they are made, and the author and Manchester Capital assume no duty to and do not undertake to update forward-looking predictions or statements. Forward-looking predictions or statements are subject to numerous assumptions, risks and uncertainties, which change over time. Actual results could differ materially from those anticipated in forward- looking predictions or statements. As with any investment, there is the risk of loss.

It is once again that most joyous time of year where we step back to take time with our families, reflect on the accomplishments of the year that has...

For ultra high-net-worth (“UHNW”) families, integrating health into wealth planning isn’t optional — it’s essential for legacy,...

Can you invest in a way which is environmentally and socially conscientious while still producing solid returns? ESG—shorthand for Environmental,...