As we write this, the S&P 500 is down 7%, the MSCI All-cap World Index is down 8%, the Bloomberg Aggregate Bond Index is down 7%, the Wilshire U.S. Real Estate Investment Trust Index is down 4%, and the HFRI Fund of Funds Composite Index is down 3%. Stocks, bonds, real estate, and hedge funds all have negative year-to-date returns. Even cash is losing purchasing power with inflation running at 7.9%. So, what is an investor to do? We have two suggestions.

First, stick to your long-term plan. The history of the market has shown, repeatedly, that while crises come and go, mankind and the market demonstrate resilience and progress.

Diversification may feel irrelevant when every asset class, sector, and subsector of the market are experiencing negative returns, and short-term losses can feel painful. It is important to have an adequate supply of short-term cash to meet short-term withdrawal needs to avoid forced sales.

Second, market declines like the one we are currently experiencing are not without opportunity. Now is a great time to harvest capital losses and to review possible estate planning moves like Roth IRA conversions, GRATs, and/or transfers of undervalued securities.

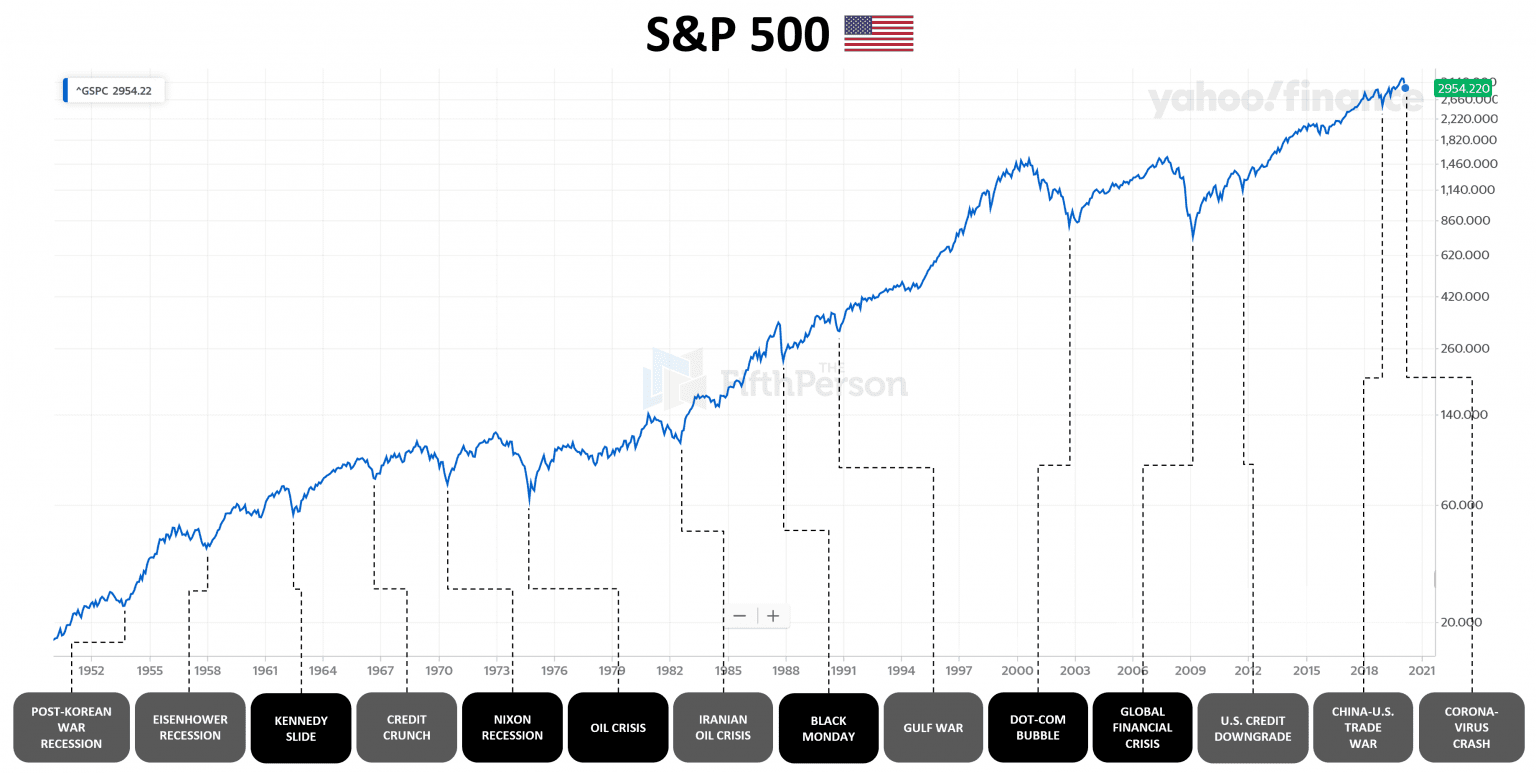

Roth Conversions involve taking a large one-time tax hit. Despite significant discussions in 2021 of raising individual tax rates, Congress never acted, and with midterm elections coming up in November, it is unlikely that tax rates will increase this year. At today’s reduced investment values, now may be a great time to convert IRAs to Roth IRAs. Taxable income will be less than it would have been at year-end, and if the above chart’s pattern holds, those reduced asset values should eventually grow under a Roth’s “never to be taxed again” umbrella.

Similarly, using some or all of one’s lifetime gift exemption to give to heirs, individuals, or irrevocable trusts for the benefit of others can exploit the same advantage—current values are depressed, so you can give away a lot more shares at today’s prices, tax-free. Additionally, an individual’s lifetime gift exemption increased to $12.06MM for 2022. Even if you had previously utilized all $11.7MM of your exemption, consider using this year’s additional $360K. This limit is still set to expire and reset to $5.49MM at the end of 2025.

Many investors realized significant gains in 2021—the result of strong market performance, mutual fund distributions, and pre-emptive sales based on Congressional interest in raising the capital gains tax rate. Like individual income tax rates, the plans to raise capital gains rates never materialized and look unlikely to change this year. With the market down, however, there are most likely tax losses that can be harvested. There are two main strategies for capturing tax losses—capture immediately or add to positions and harvest the positions with losses later.

The “wash-sale” rule prohibits investors from capturing a tax loss if proceeds from a security sale are reinvested in a “substantially identical” security within 30 days. You can, however, switch to relatively similar funds, indexes, and Exchange Traded Funds (ETFs) offered by different providers. This allows you to maintain a reasonably similar exposure while capturing valuable tax losses to offset future gains. An alternative is to add to positions where you have existing losses. Then, after the 30-day wash-sale period, sell the position with the loss. Unused capital losses can be carried forward to offset losses indefinitely.

At Manchester Capital, while we work hard to determine asset allocations and identify outstanding managers in search of superior investment returns, we recognize that wealth transfer strategies, trust strategies, and tax strategies like Roth conversions can add significant value and help clients achieve their long-term objectives. If you would like to discuss the feasibility of any of these strategies with your wealth manager, please feel free contact us.

Disclosures

This material is solely for informational purposes and shall not constitute a recommendation or offer to sell or a solicitation to buy securities. The opinions expressed herein represent the current, good faith views of the author at the time of publication and are provided for limited purposes, are not definitive investment advice, and should not be relied on as such. The information presented herein has been developed internally and/or obtained from sources believed to be reliable; however, neither the author nor Manchester Capital Management guarantee the accuracy, adequacy or completeness of such information.

Predictions, opinions, and other information contained in this article are subject to change continually and without notice of any kind and may no longer be true after any date indicated. Any forward-looking predictions or statements speak only as of the date they are made, and the author and Manchester Capital assume no duty to and do not undertake to update forward-looking predictions or statements. Forward-looking predictions or statements are subject to numerous assumptions, risks and uncertainties, which change over time. Actual results could differ materially from those anticipated in forward- looking predictions or statements. As with any investment, there is the risk of loss.

It is once again that most joyous time of year where we step back to take time with our families, reflect on the accomplishments of the year that has...

For ultra high-net-worth (“UHNW”) families, integrating health into wealth planning isn’t optional — it’s essential for legacy,...

Can you invest in a way which is environmentally and socially conscientious while still producing solid returns? ESG—shorthand for Environmental,...