The Federal Reserve finished their latest Federal Open Market Committee (FOMC) meeting on June 12th and as expected, held the benchmark interest rate (the federal funds rate) unchanged at 5.25 – 5.50%. During the press conference after the meeting, Fed Chairman Powell stated, “We are maintaining our restrictive stance of monetary policy in order to keep demand in line with supply and reduce inflationary pressures. We are strongly committed to returning inflation to our 2% goal and supportive of a strong economy that benefits everyone.”

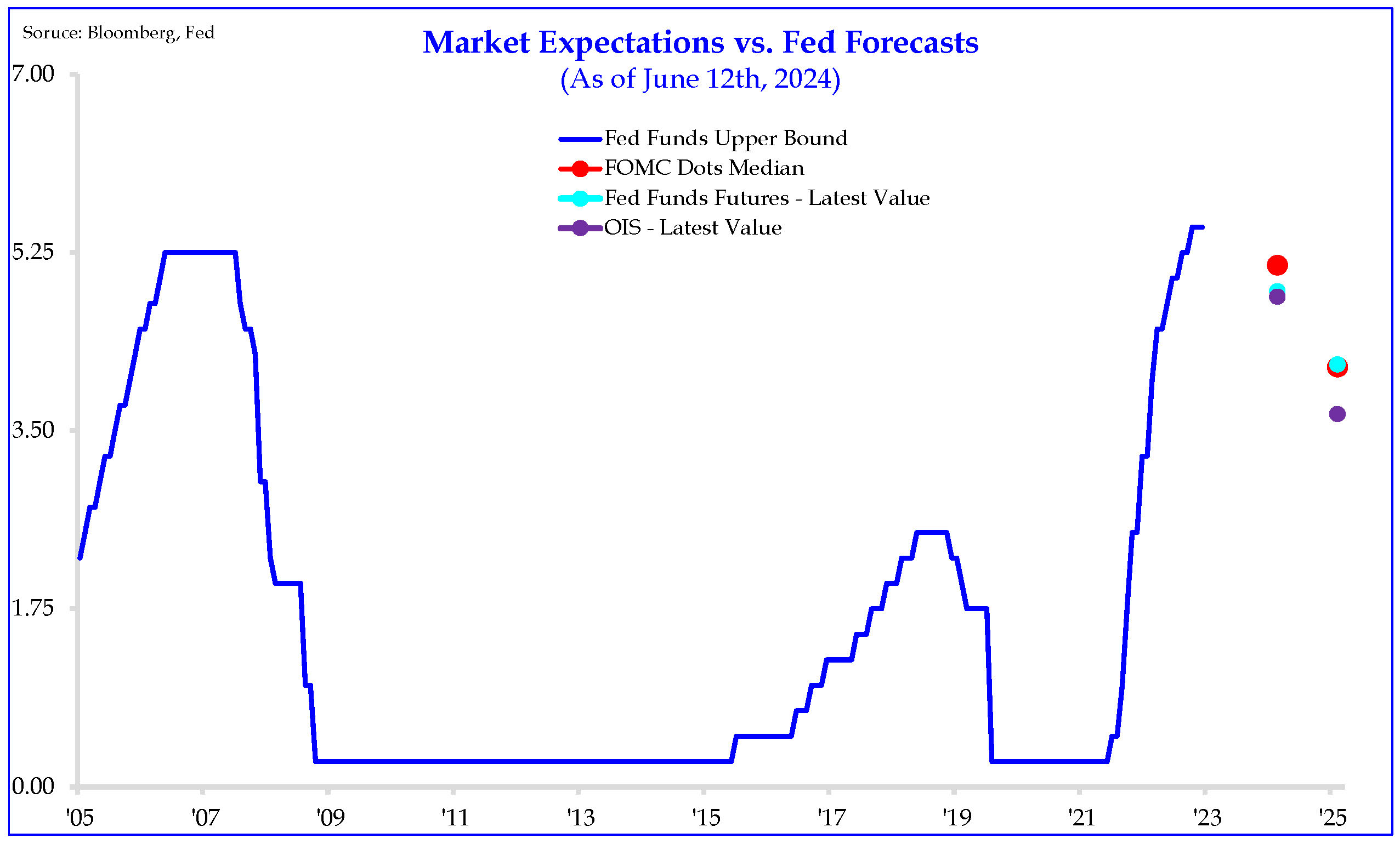

Given all the economic and inflation data available, the Fed is now projecting just one rate cut this year, which generally means a modest 0.25% cut to 5.00 – 5.25%. Of course, if inflation eases below 3% and/or unemployment rises above 4%, then the Fed may look to act sooner. When the Fed’s inflation and employment targets are met, their longer-range projection is to ease rates down to their target range of 2.50% to 2.75%.

Higher than acceptable inflation is one of the two factors keeping the Fed from lowering rates. The latest inflation reading was 3.3% and the latest core PCE Price Index reading (the Fed’s preferred metric) was 2.8%. Both inflation gauges have eased since peaking 2 years ago but are still above the Fed’s target of 2.0%. While many components of the inflation rate have fallen to within the Fed’s target, shelter and transportation services remain stubbornly high. Shelter, representing 34% of the CPI, has been slower to cool than many other components. The cost of owning a home is a big component of shelter and is represented by the rents charged on comparable homes, a measure called owners’ equivalent rent. This data is sticky and lags other more quantifiable inflation components.

The strong labor market is the second factor keeping the Fed from lowering rates. The latest report from the Bureau of Labor Statistics showed the economy generated 272,000 jobs in May, mostly in healthcare, government, technical services, and leisure and hospitality. The report indicates the unemployment rate rose modestly to 4%. Although this rate is still below the “natural rate” of unemployment, it has been slowly climbing from a low of 3.4% last year.

Interestingly, interest rate cuts at the current level of inflation and unemployment are rare, according to Strategas Research. Strategas reviewed the previous 100+ rate cuts that occurred since 1972. While about 30% of cuts occurred with inflation rates below the current 3.3% level, there have been just 6 cuts when the unemployment rate was below 4%. This suggests investors should be more focused on labor now, which may start weakening as corporate borrowing slows. Interest rate policy decisions have a significant impact on business investment decisions. Corporate borrowing costs are influenced by changes in interest rates. Higher rates may discourage expansion plans and capital expenditures, while lower rates can lower the cost of capital and encourage investment in new projects and equipment.

It is also important to remember this is a presidential election year. A review of monetary policy decisions since 1972 shows that the Fed has historically eased during election years. As such, we are expecting the first rate cut to come on September 18th, the last FOMC meeting before the November election.

There are reasonable concerns among investors and economists that inflation could reaccelerate. In the past, when the Fed began an expansionary monetary policy by lowering interest rates, it was rare for inflation to be higher 12 months later. In fact, the only instance when inflation was higher 12 months after the initial rate cut was during the 2008 financial crisis. This could have been because energy prices increased 20% over the same period. While there is no precedent for the current economic conditions, history would suggest the probability of a re-acceleration of high inflation over the next year is minimal.

Investors are eagerly awaiting the start of a Fed easing cycle because lower rates benefit stocks, bonds, the housing market, and the economy writ large. Lower rates are coming but investors might need to be a little more patient. We are expecting “higher for longer” interest rates, meaning, we expect interest rates to remain high throughout this year and 2025, with the short end of the yield curve only dropping about 1% to 4.5% over the next year. Over this same time period, we expect longer-term rates to normalize, which means they would decline slightly from current levels but remain within historic ranges. The 10-year Treasury, currently yielding 4.30%, would be less elastic, falling 30 to 40 basis points to just under 4%.

Many investors believe longer-term rates will fall more, returning to the levels experienced over the last decade. While this could be true, it may also show some anchoring bias on the part of fixed income investors. They may have been spoiled with 0% interest rates for 9 of the last 15 years, resulting in an average Fed funds rate of just 0.4% from the 2008 financial crisis until the Fed started its record-breaking interest rate hiking campaign in 2023. During those 15 years, consumers gorged themselves at the trough of easy money, enjoying short term borrowing rates as low as 0.50% for margin loans and near 3% for long-term mortgages. We would argue that the current yield on the 10-year Treasury of 4.3% is quite normal and emblematic of a normalized yield curve—one for which the long-term average yield is 4.25%—but that would put us in the middle between history and today’s investors’ voracious appetite for cheap funds.

We are mindful that once the Fed starts cutting interest rates, the dollar should weaken against other major currencies (all else being equal), which bolsters the dollar-denominated returns from our foreign investments. It is also worth noting the concept of the “Fed Put”. There is a popular belief that if the economy slips into a recession, or if there is a major shock to the market, the Fed will come to the rescue and immediately lower rates to zero or close thereto. With, or without, a shock interest rates are heading lower, it may just take longer than economists and the Fed led investors to believe.

Disclosures

This material is solely for informational purposes and shall not constitute a recommendation or offer to sell or a solicitation to buy securities. The opinions expressed herein represent the current, good faith views of the author at the time of publication and are provided for limited purposes, are not definitive investment advice, and should not be relied on as such. The information presented herein has been developed internally and/or obtained from sources believed to be reliable; however, neither the author nor Manchester Capital Management guarantee the accuracy, adequacy or completeness of such information. Predictions, opinions, and other information contained in this article are subject to change continually and without notice of any kind and may no longer be true after any date indicated. Any forward-looking predictions or statements speak only as of the date they are made, and the author and Manchester Capital assume no duty to and do not undertake to update forward-looking predictions or statements. Forward-looking predictions or statements are subject to numerous assumptions, risks and uncertainties, which change over time. Actual results could differ materially from those anticipated in forward-looking predictions or statements. As with any investment, there is the risk of loss.

It is once again that most joyous time of year where we step back to take time with our families, reflect on the accomplishments of the year that has...

For ultra high-net-worth (“UHNW”) families, integrating health into wealth planning isn’t optional — it’s essential for legacy,...

Can you invest in a way which is environmentally and socially conscientious while still producing solid returns? ESG—shorthand for Environmental,...