Information and education are an essential part of the client experience, and we

are here to provide resources and insights to help keep you advised.

It is once again that most joyous time of year where we step back to take time with our families, reflect on the accomplishments of the year that has passed and we, the authors, have the pleasure of writing another “By the Numbers” article. This year we saw the impact of tariffs, attempted and actual assassinations, hostage releases, space rescues, a Chicago Pope, airplane crashes, wildfires, wild swings in the market, a government shutdown, deportations, protests, and the ever-evolving world of artificial intelligence that made 2025 one for the books. Here are some numbers that help to tell that story: $18.81 Trillion – Dollars invested in ETFs globally. Assets have increased 26.7% year-to-date.1 $878 Billion – Dollar value of Elon Musk’s pay package at Tesla, approved by shareholders in November. In order for Musk to realize the full amount, Tesla market capitalization must rise in value from $1.5 trillion to...

09.18.2023

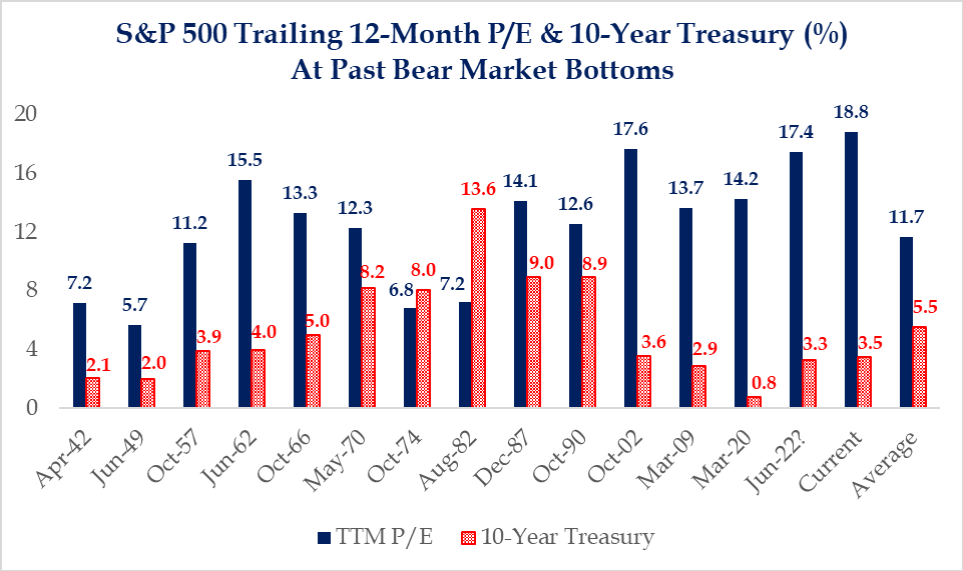

The year 2022 was a bloodbath for both equity and bond markets–the S&P 500 was down 18% and the Bloomberg US Aggregate Bond Index had its worst year ever, down 13%. This year, 2023, began with the US debt ceiling standoff, followed by a banking crisis, and continued rate hikes by the major central banks. The economy seemed like it would get worse before it got better, and the consensus was calling for a near-term recession. However, the stock market quickly shrugged off many of these concerns. Year-to-date as of August 31, the S&P 500 is up approximately 17% and NASDAQ is up approximately 34%. The S&P 500 is officially in a bull market (i.e., up at least 20% from its recent lows in October 2022). With the Federal Reserve and some economists no longer forecasting a recession[1], it makes one wonder what has changed in the last few months....

Following the collapse of Silicon Valley Bank and Signature Bank, banking regulators appeared on Capitol Hill last week. Fed Vice Chair for Supervision Barr and FDIC Chair Gruenberg testified before the Senate Banking and House Financial Services Committees about the recent bank failures. The Federal Deposit Insurance Corporation estimates it will cost $22.5 billion to backstop both Silicon Valley Bank and Signature Bank, guaranteeing all deposits. After the initial shock of these bank failures and the heightened sensitivity around bank holdings, the market rapidly adjusted to the new risks with the quickest monetary tightening in 44 years. Still, banks face several headwinds. First, the yield curve remains inverted—longer-term interest rates are lower than short-term rates. For example, the 10-year Treasury is yielding 3.38%, while the Fed Funds rate is 5%. This inversion is the largest in 42 years. It is generally viewed as a bearish signal for the economy,...

“If you mix politics with your investment decisions, you are making a big mistake. Each generation of Americans has been, and will continue to be, better off than the previous generation.” - Warren Buffet

"The Federal Reserve, after delaying for more than a year claiming inflation was 'transitory,' has finally embarked on a serious course to bring inflation under control."

"Transferring wealth during periods of depressed asset values, like coiling a spring, allows for the passing of assets with the potential to expand when the market recovers (as markets have historically always done)."

"Although the current market correction is unsettling for investors, it also presents opportunities for long-term investors who can stay invested and adjust as the cycle changes."

"Stocks, bonds, real estate, and hedge funds all have negative year-to-date returns. Even cash is losing purchasing power with inflation running at 7.9%. So, what is an investor to do?"